A good credit score is important when it comes to getting a mortgage, car loan, or personal loan. Credit agencies like to see that you are responsible when it comes to managing your debt. A young person might only have one credit card while someone 40 years old may have multiple credit cards, a mortgage, and a car loan. It is also important to avoid opening new credit accounts because they will lower your score. Although a new account may result in a hard inquiry on credit reports, it will usually disappear within one-year.

Recent college graduates have an excellent credit score

Many financial milestones await college graduates in their adult lives. Many of these milestones may be difficult to achieve for people with low credit scores. Many lenders, insurers, and employers will base their decisions on your credit history, so it is important to establish a good score early. Bad credit can make it more difficult to obtain large loans, good car insurance rates, or even get utility service.

Recent college graduates have an average credit score of 689. This score is 12 points lower than the national average. This is a great score for young people. However it will cost you more to get into the higher tiers.

To maintain a high credit score, keep your credit utilization low

Keep your credit utilization ratio low to increase your credit score. This will make your credit more attractive to lenders. It can also help you obtain better rates and larger loans. A good place to start is to keep your credit utilization under 30 percent. It is not a perfect science.

Credit utilization refers to the percentage of credit that you use. It makes up 15% of your FICO Score. A good score is achieved by keeping this ratio below 30 percent. A credit card application is one of your best options to lower your utilization. This will also boost your total credit line.

Another important way to improve your credit score is to pay off your credit cards on time. Lenders will use your credit utilization rate to determine your repayment risks. High credit utilization means you're more likely to overspend than you are, while a low credit utilization rate indicates you're a responsible credit user.

Reliable financial practices can increase your credit score.

Reliable financial habits are the best way to improve your credit score. This includes paying your bills in time and maintaining a low credit usage ratio. You should also avoid maxing out new credit accounts. If you are responsible, your credit score will rise quickly. But, you may experience a rapid decrease in credit scores if it is difficult to pay your bills.

Your credit score is 35 per cent dependent on your payment history. Therefore, it is important to pay your bills on time. This will demonstrate to creditors that your repayment history is accurate and that you will adhere to the payment deadlines. Don't forget to pay your credit card bills on time. Missing even one payment will damage your credit score. Do not miss any payments.

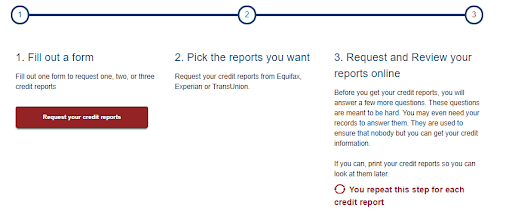

The credit score is used by lenders to determine if they are willing to lend you money. Your score ranges from 300 to 850, and it can be impacted by different factors. For example, late payments can decrease your score by 30 points or more. The collection account will remain on your credit report even if it is paid off. It will still be on your credit report for seven years.