A prospective lender will see that you build credit steadily to show them that you can manage your finances responsibly. It is difficult to predict the time it will take to build credit. But there are many factors that can affect the time it takes for your credit score to rise.

Build credit starting from scratch

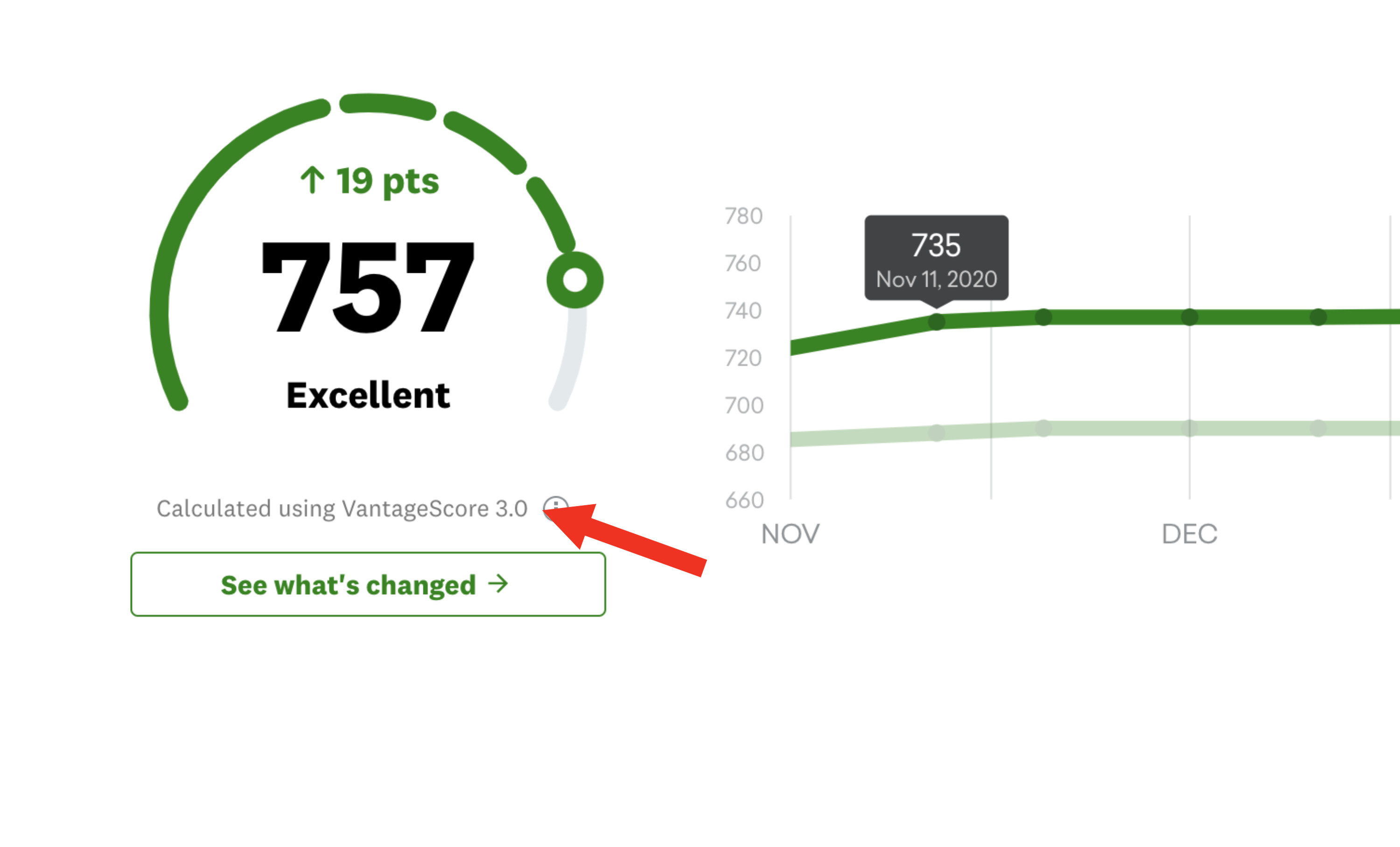

There are many options when it comes to building your credit score. A few simple strategies can help improve credit scores. These tips can help you build great credit and reap the rewards of higher credit limits, better interest rates, and credit card rewards. It can be time-consuming to build your credit score. However, with the right strategy, you can see improvements in just a few short months.

Establishing a credit history is the first step in building credit. It involves opening an account and reporting it the U.S. consumer credit bureaus.

New accounts opening

Open new credit accounts can negatively impact your credit score. Although this effect is often temporary, it can sometimes last up to a year. The impact depends on the type of credit score you have, but generally, a new account will lower your score by 6 to 12 points. FICO credit scores can range between 300 and 850. Most people fall between 600 to 750. While new accounts can negatively impact your credit score, they can also have a positive effect if payments are made on a timely basis.

It is best to limit how many accounts you open when applying for credit. A low credit score can impact your credit score temporarily, but can improve over time. It's best to start off with a few smaller accounts, and make sure to manage them responsibly for a year or two.

Payment history

It is essential to pay your bills in time to build a strong credit history. You can keep your credit score strong by paying your bills on time. Bankruptcies and missed payments will remain on your credit report for 7-10 years. Follow these guidelines to quickly establish a positive payment history.

Your first step is to begin paying your delinquent account. You should catch up on any late payments and arrange to make your future payments on time. You won't lose your late payments but your overall payment history will be affected.

Rate of credit utilization

Your credit utilization rate is one of the most important aspects of your credit score. A low credit utilization rate makes you more attractive to lenders, which can lead to higher interest rates and greater loans. Fortunately, there are many ways to improve your credit utilization rate. It is important to use as little credit as you can.

The credit utilization rate, which is the ratio of your credit use to total credit available, is a number. If your credit utilization ratio is lower than 30%, then you're on track. This number is crucial because it can greatly improve your credit score.