Many financial experts recommend that customers regularly review their credit reports. In fact, the process is free. It's a good idea to do this each year. Afterward, it's a good idea for any mistakes to be fixed. This should be at the top of your "To Do” list. It is important to know the specific areas on your report.

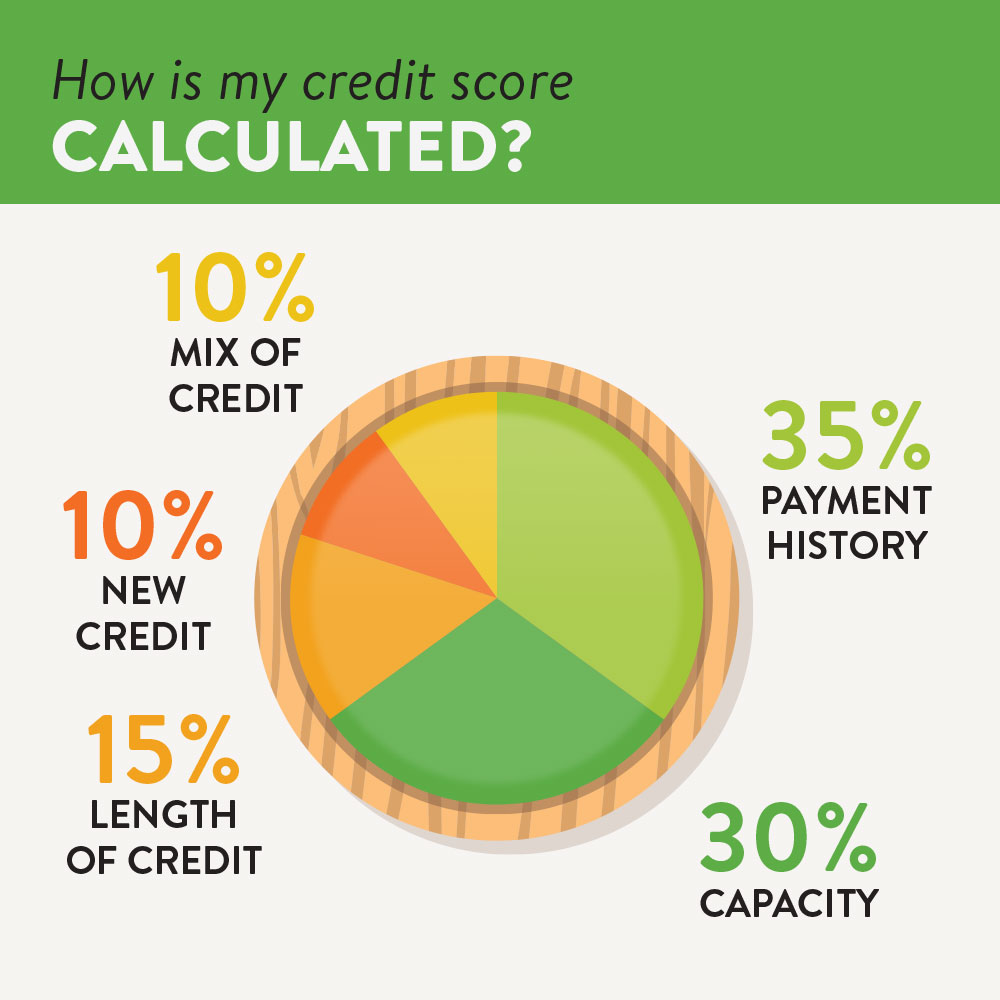

History of payments

A credit report includes important data such as the payment history for accounts. This information shows late payments and their severity. Your score will be affected based on the severity and frequency of late payments. The more recent the payments were, the better. A positive payment history is generally a sign that consumers are making their payments on-time.

Your payment history will improve if you make your payments on-time. Even though it will require sacrifices at times, it is necessary to establish a positive record of payments. Even if your accounts are spread across multiple accounts, make sure to pay all bills on time every month. You may find it helpful to use autopay or to set up reminders on your calendar to remind you to pay your bills. If you're having difficulty paying your bills, it may be time to review your spending habits.

Credit history length

Your credit score is affected by the length of your credit history. Your credit score is more important if your credit history is longer. This is calculated by looking at the average age of all your accounts. The report shows older accounts that are longer than those of newer accounts.

By adding up all your accounts, and dividing by the number year you have been using them, the length of credit history can be calculated. You can cut your history's average length by half by opening a new bank account. Additionally, a new account creates a hard inquiry on your credit report. This hard inquiry should be considered when you apply for credit. A hard inquiry can lower your score considerably, so it is important to act quickly to recover.

New credit

When applying for new credit, it is important that you are clear about what inquiries may be in your report. While it's possible to make several inquiries at one time, credit scoring mavens tend to count them as one if they are made within a certain time period, which can vary from fifteen to 45 days.

Different types of credit

Credit files contain detailed information about your borrowing patterns. Consumer-credit agencies (CRAs) keep separate files for each consumer. Lenders and merchants use this information to evaluate your risk. These data help determine the risk of lending to you.

Age of the account

Your credit score may be affected by how old your credit history is. Your credit score will go up the more you have credit history. Calculating your account age involves taking the average age across all accounts and then dividing it by how many accounts you have. It is also important to have a mix of old and new accounts, as this will demonstrate how you have managed different types of debt. FICO or VantageScore can be used to calculate credit scores.

Misinterpreting account age is one of the biggest mistakes people make. In reality, there are a number of factors that influence account age. It is important to understand the implications of each factor on your credit score.