If you have ever wondered what your credit score is, you aren't alone. ZILLOWPOPULATIONSCIENCE states that the average American is only able to understand two things about credit scores. And that gap is spanning all age groups. Boomers and Gen X were less familiar with credit than Gen Z. Continue reading to find the answers you need about credit scores.

Common questions regarding credit scores

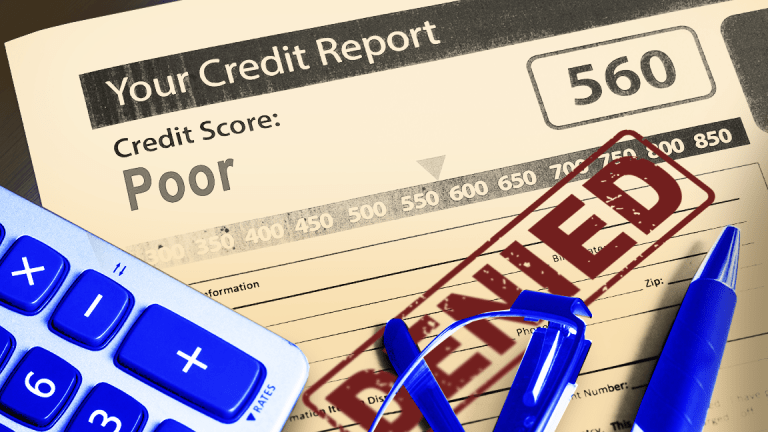

Your credit score could make a huge difference in your ability to apply for loans or apartments. If you're serious about reaching your financial goals it's crucial to understand what it is. Credit scores are affected by several factors, such as credit utilization and payment history. Lenders also use your score to determine how likely you will be to repay future loans.

How to find your score

The credit score is a number that lenders use when deciding whether you are a suitable risk to lend money. It can range between 300 and 850. This score tells lenders whether or not you will be able repay loans. The score is affected by your credit history, so it's important to keep track of it regularly.

Hard inquiry vs. easy inquiry

There are two types if inquiries that you can make on your credit report: a hard inquiry or a soft inquiry. Each type of inquiry has a different impact on your credit score. When you apply for a loan such as a car loan or student loan, a hard inquiry is made. Depending on your credit history, a hard inquiry may lower your credit score by 0-5 points. This means it's important to stop applying for credit if you don’t need to.

Impact of hard inquiry on your credit score

A hard inquiry is triggered on your credit report when you apply to borrow money. Hard inquiries indicate to potential lenders that you are actively seeking credit. This will hurt your score because it will appear on your report, regardless of whether the application is approved or rejected. Hard inquiries can also indicate that you have applied credit within the last two-years.

Getting a good credit score

One of the most important aspects of maintaining a good credit score is paying your bills on time. If you're late on one or more payments, it will reflect negatively on your credit score. Paying your dues is what will determine more than 30% of your credit score. You can avoid falling prey to the temptation to neglect to pay by setting up automatic payments.

Before you apply for a loan, know your score

Before applying for a loan you should know your credit score. This can impact your application. It provides information about how you manage your finances. Most lenders look at your score to determine your repayment habits. However, credit scores are only one piece of the puzzle. Lenders also take into account your income, which can affect your score. It is possible to spot red flags in your credit score and avoid being taken advantage.