Credit scores are determined by what type of credit you have. This "credit mix" is also known as your credit score. You can have "good", which means mortgages, and "bad", which means high-interest credit card debts and payday loans. Your score will be affected by the type of credit you have. It is important to know what factors will impact your score.

Credit history length

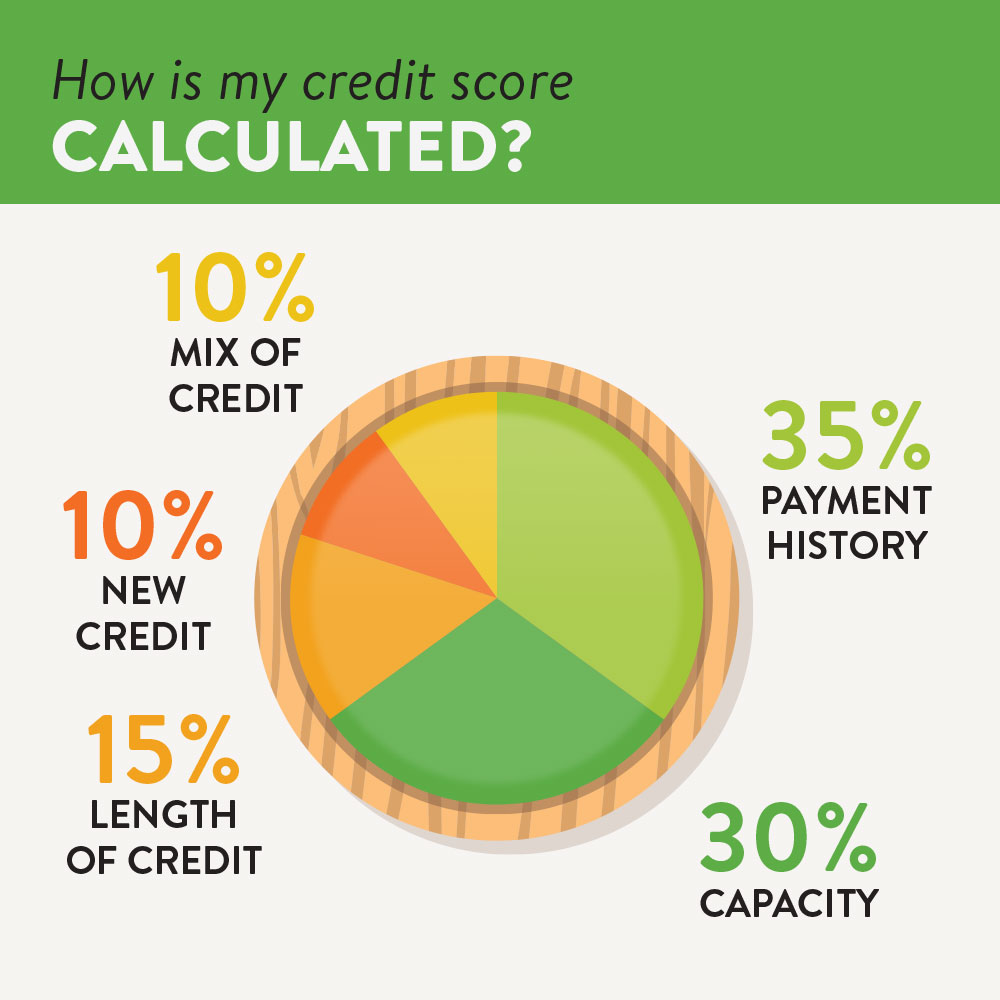

The length of your credit history is an important factor when it comes to your credit score. This is the average age for all your credit accounts. Credit scoring agencies calculate it. Your credit history will determine how high your score. A short credit history does not mean you cannot have good credit. A good way to build credit is to make on-time payments and avoid late payments.

The length of your credit history is one of the five major factors that impact your score. It's in the middle, between the age of accounts and the amount you have used of credit. Your credit history should be longer, but you also need to consider other factors. People with good credit have an average score of 711 and having a longer credit record can help you keep a good score.

Payment history

Credit score is largely determined by your payment history. Lenders use this score to make lending decisions. Your score can be hurt if your late payments are frequent. Pay your bills promptly and in full to improve your score.

Your payment record shows which accounts were your responsibility and when. This information contributes 35% to your credit score. Because this information tells lenders how likely they are that you will pay your debts, it is important for them to prioritize your payment record. It is important to remember that late payments won't automatically lower your credit score. Your positive payment history may outweigh the few late payments.

Credit utilization

Credit utilization ratio is a key factor in determining your credit score. This can help you determine if you are a high-spending customer or a low risk customer. It can also increase your chances of being approved for a loan. In general, you should limit your credit limit to revolving account usage to less than 30 percent. It is important to pay your monthly balances. To get a better view of your credit utilization, you can access your credit score online.

Your credit score will drop if you have a high credit utilization. Having a balance-free credit card may be one way to boost your score. A high balance on your credit card can have a negative impact on your credit utilization ratio. Paying your balances in a timely manner can help you improve your credit score.

Credit utilization doesn’t include collections

Credit utilization is an important component of your credit score. It shows the scoring model how well credit management is going. Your score can be affected if you have high credit utilization. The best thing for your credit score is to keep it below 30%. There are several factors that impact your credit utilization. One example is if you have too many credit cards, or too few loans.

Remember that credit card debt represents a small portion of your total credit limit. If you only use a small amount of your credit, collections should not be a concern. Even if there are several high-limit credit cards available, your total utilization ratio should be below 30%. This will allow you to have thousands of dollars in available credit.

VantageScore

A VantageScore is determined by your payment history. It shows lenders that the borrower can handle different types of credit. You will reduce your credit utilization and increase your score by paying off your debts promptly. It is a good idea not to close your oldest credit accounts.

VantageScore takes into account several factors such as your payment history and total debt. Your payment history is responsible for around 35% of your score. However, the percentage of total debt owed is also important. Your credit utilization plays a big role. It's generally a good thing to keep your credit limits to 30% or lower.